Plan your dream work/life balance and save up to RM3,000* in tax relief

Secure your retirement and reduce taxes by investing in Private Retirement Scheme (PRS)! Get RM50* bonus when you invest in Private Retirement Scheme via Versa. T&Cs apply. Learn More Here >

Get to know Private Retirement Scheme

Private Retirement Scheme (PRS) is a voluntary investment scheme designed to help you accumulate savings for retirement. It is a great complement to your Employees Provident Fund (EPF)!

Begin your retirement journey with AHAM Capital's Private Retirement Scheme.

We aim to help you

Build your retirement fund, save on taxes

Let's find out how much tax savings you can save with your estimated annual taxable income!

![]() Annual taxable income is the total of your annual income after deducting personal tax reliefs

Annual taxable income is the total of your annual income after deducting personal tax reliefs

ENTER YOUR ESTIMATED ANNUAL TAXABLE INCOME

RM

GET INCOME TAX SAVINGS OF

RM 0

If you invested RM 3,000 in Private Retirement Scheme based on your 0% tax bracket. (Note that this can only be claimed on the following year when you file your income tax)

That’s

packs of nasi lemak!

Enjoy Income Tax Relief

Claim up to RM3,000 in income tax relief, growing your personal cash flow.

Expand Your Retirement Plan

Experience the flexibility of voluntary contributions and diversify your retirement income with ease.

What Is a Private Retirement Scheme (PRS)?

A Private Retirement Scheme (PRS) is a voluntary long-term savings scheme introduced to help Malaysians build additional retirement funds. With Private Retirement Scheme, you can decide how much to contribute, making it a flexible solution for long-term financial planning.

Private Retirement Scheme contributions are channelled into approved Private Retirement Scheme funds, allowing individuals to grow their retirement savings in Malaysia over time. Private Retirement Scheme contributions are channelled into approved Private Retirement Scheme funds, allowing individuals to grow their retirement savings in Malaysia over time. Users can choose from different conventional or Shariah-compliant options depending on their preferences.

How Private Retirement Scheme Works in Malaysia

Private Retirement Scheme operates through a structured and regulated framework designed to support

long-term retirement planning.

Complementary to EPF

Private Retirement Scheme complements EPF by allowing voluntary contributions that support long-term retirement planning in Malaysia.

Voluntary Contributions

Contributions are voluntary with no maximum limits, allowing individuals to contribute based on their financial capacity.

Investment Into Private Retirement Scheme Funds

Private Retirement Scheme contributions are invested in professionally managed funds that use different investment strategies, from conservative to growth-oriented.

Tax Relief for Malaysians

Private Retirement Scheme contributions are eligible for up to RM3,000 in annual tax relief, supporting Malaysians who are planning their long-term retirement savings.

Private Retirement Scheme and EPF can work together within a long-term financial plan. EPF offers structured, employment-based contributions, while Private Retirement Scheme provides a voluntary option for Malaysians who want to set aside extra funds to grow their retirement savings. This makes Private Retirement Scheme complementary to EPF for individuals who want more control over their retirement strategy.

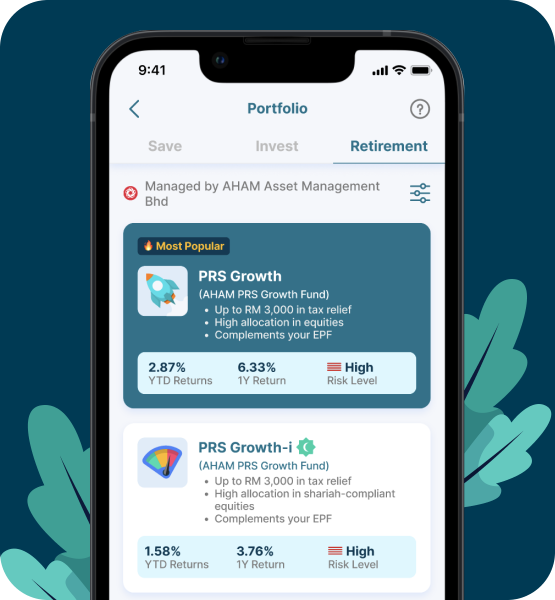

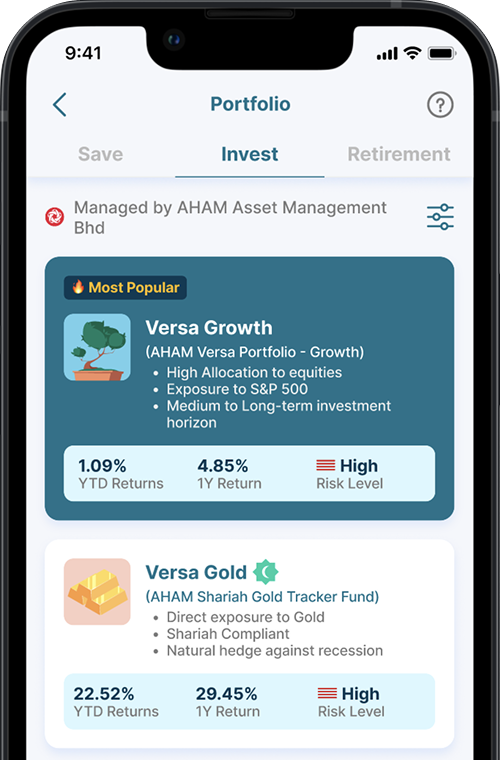

Explore our offerings

Choose from an array of funds to meet your retirement needs, goals and risk appetite:

PRS Growth

AHAM PRS Growth Fund

Retirement fund focused on capital growth

Risk Level: High

PRS Moderate

AHAM PRS Moderate Fund

Retirement fund focused on income & capital growth

Risk Level: Moderate

PRS Conservative

AHAM PRS Conservative Fund

Retirement fund focused on capital preservation

Risk Level: Low

PRS Growth

AHAM PRS Growth Fund

Retirement fund focused on capital growth

Risk Level: High

Versa Moderate

Equities focused fund for higher potential returns

Fund Type: Growth

Risk Rating: High

Versa Moderate

Equities focused fund for higher potential returns

Fund Type: Growth

Risk Rating: High

Why Use Private Retirement Scheme for Retirement Planning in Malaysia

Private Retirement Scheme appeals to Malaysians who want more flexibility and control over how they build their long-term retirement savings. Beyond its basic structure, Private Retirement Scheme supports financial habits and planning needs that evolve throughout different life stages.

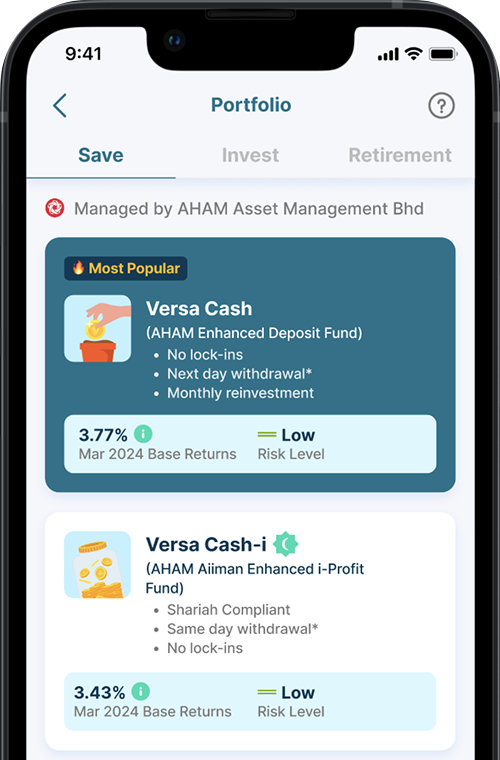

Explore Our Other Solutions

Versa Save

Earn higher returns than your traditional savings account from just RM10!

Recent Articles

Recent Articles

Understanding Risk Levels of Investment Options in Malaysia

May 7, 2026

Savings Plans in Malaysia: Overview and Strategies

May 6, 2026

Choosing an Investment App in Malaysia That Fits Your Needs

May 5, 2026

Is RM1 Million Enough to Retire in Malaysia?

April 20, 2026

Your Goal Tracker Just Got a Major Upgrade! 🚀

April 20, 2026

💸 Transfer Your PRS Balance & Get Rewarded

April 3, 2026

2026 Versa Starter Quests for April New Joiners!

April 1, 2026

Adulting Can Be Too Much. So, Let Us Pay Your Bills!

February 10, 2026

All New 2026 Invest Booster Quest

January 1, 2026

Versa Malaysia Bond: Increase resilience with Malaysia Bonds

August 4, 2025

Versa China Equity Tracker: Invest in China’s New Economy

May 1, 2025

Versa India Equity: Invest in India’s Rise

May 1, 2025

Ride the Tech Wave: Introducing Versa US-Tech

February 19, 2025

KJ x Versa Quests: How I’m Empowering Malaysians to Take Control of Their Finances

October 17, 2024

Stack and earn 9%* p.a. or more nett returns with Versa Quests!

July 5, 2024

Frequently Asked Questions

If you are a new Versa user interested in Private Retirement Scheme (PRS), you will have the option of investing in Private Retirement Scheme during our onboarding process.

For existing users, you can begin onboarding by answering one question about your monthly household income. After that, approval will take approximately 5 days. Once approved, you can start investing in Private Retirement Scheme and enjoy the benefits of our retirement scheme!

Yes, you may invest in multiple Private Retirement Scheme funds at the same time.

Yes, under Private Retirement Scheme, there are different rules regarding the cash outs of funds based on two separate accounts: Account A and Account B.

For Account A, cash outs can only be made upon reaching the retirement age specified by the Private Retirement Scheme provider.

Whereas for Account B, you are allowed for one cash out per calendar year. However, if you are below 55 years old, this withdrawal from Account B is subjected to an 8% tax penalty, unless the purpose of the withdrawal is specifically for housing or health-related expenses.

The Versa platform does not charge any fees to their user. However, there are management fees, trustee fees and fund-level fees paid to the fund managers, which differs based on the portfolios.

Please refer to respective prospectus.

The minimum contribution limit for Private Retirement Scheme (PRS) in Malaysia is RM 100. As for the maximum contribution limit, there is generally no specific maximum limit set for Private Retirement Scheme contributions per transaction. However, it is important to note that the maximum contribution amount may be subject to the limits imposed by FPX (Financial Process Exchange), which is RM 30,000.

You can track the performance of your Private Retirement Scheme investment in our app’s fund overview dashboard.

Private Retirement Scheme (PRS) is a voluntary retirement savings scheme, while EPF is mandatory for employees in Malaysia. Private Retirement Scheme complements EPF by providing an additional way for individuals to contribute toward long-term retirement planning at their own pace.

At age 55, individuals may withdraw their full Private Retirement Scheme balance without penalties as part of the retirement process. Private Retirement Scheme providers will outline the options for redemption and the required documentation.

Private Retirement Scheme funds typically follow different investment strategies, such as conservative, moderate or growth-oriented approaches. Each strategy has its own asset allocation and risk profile, which are disclosed in the fund’s prospectus and fact sheet.

No. Private Retirement Scheme funds are invested in capital market products, which means their value may fluctuate based on market conditions. Individuals should review each fund’s objective, allocation and risk profile before contributing.

Private Retirement Scheme provides a structured framework that encourages long-term savings by limiting early withdrawal and supporting consistent contributions. Over time, this helps individuals accumulate additional savings alongside EPF.

Yes. Many Private Retirement Scheme providers offer Shariah-compliant funds that follow Islamic investment principles. These funds are suitable for individuals who prefer Shariah-aligned retirement planning options.